Yemi Cardoso, Governor of the Central Bank of Nigeria was guest of the Harvard Club of Nigeria in Lagos on Friday October 4th, 2024.

In speaking to the topic – “Leadership in Challenging Times: Restoring Credibility, Building Trust, and Containing Inflation”, he referenced the raising of the MPR from 18.45% in February 2024 a few months after he assumed office to the current level of 27.25% on September 24th, 2024.

According to a report, he told his audience that “Our decision to raise the Monetary Policy Rate (MPR) to 27.25% was a bold move. Higher interest rates, while painful for borrowers, are necessary to curb excess money in circulation and control inflation. Leadership is about making hard choices to secure long-term stability over short-term comfort in moments like these.”

Reading that portion of the report from his interaction with the Harvard Club of Nigeria Yemi Cardoso’s comments about the MPR, interest rates and inflation took me many years back to when I was a Deputy Manager in the Research and Economic Intelligence Department of Zenith Bank.

In that role, the bulk of my work was routine; stock and money market monitoring and analysis as well as analysis of foreign exchange transactions and trends.

But aside from data collection and trend analysis I did some writing; producing the Zenith Economic Quarterly and analyzing feasibility studies for new businesses. It was from analyzing feasibility studies that I gained some unique insights about setting up a business and the disposition of Nigerian entrepreneurs to banks and the loans they obtain from banks. It was there I learnt about interest rates and Nigerian businesses. But I will come to that shortly.

Back then at Zenith, I recall that when I started compiling money market reports, the reference for interest rates was something called the Minimum Rediscount Rate (MRR). It was replaced on December 4, 2006 with the now popular Monetary Policy Rate (MPR).

The CBN noted at that time that “The MPR would be the main instrument of the new monetary policy framework and will determine the lower and upper band of the CBN standing facility and is expected to have the capability of acting as the nominal anchor for other rates.” That lower and upper band is what we now know as the asymmetric corridors.

The MPR is therefore a benchmark that determines the interest rate at which banks lend to their customers. Raising or lowering the MPR also has an effect on inflation by controlling the amount of money in circulation. This is why Yemi Cardoso has made it a key aspect of his inflation control agenda.

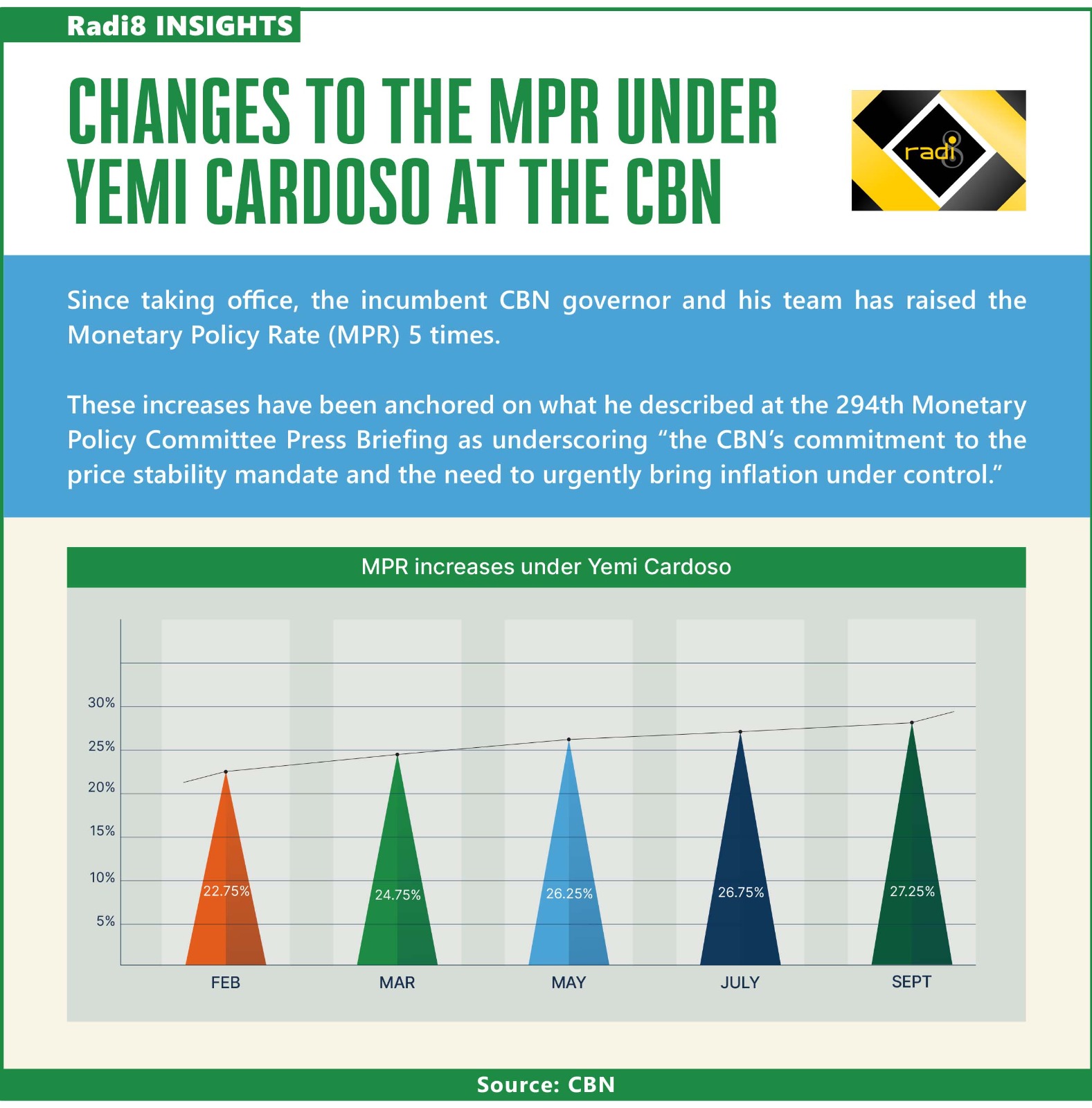

Since taking office, the incumbent CBN governor has raised the MPR 5 times.

These increases have been anchored on what he described at the 294th Monetary Policy Committee Press Briefing as underscoring “the CBN’s commitment to the price stability mandate and the need to urgently bring inflation under control to ensure that the purchasing power of ordinary Nigerians is restored in the short to medium term.”

With each raise, financial analysts and commentators have expressed their opinions. While varied, the common denominator has been the fact that a high interest rate which is correlated with a high MPR will impact the borrowing costs for businesses and individuals.

The point has also been made that the negative impact on borrowing for investment and consumption purposes could slow down economic activity but what they do not say as loudly is that a high MPR rate means that those who put their money in savings deposits or TBs will get more bang for their buck and even foreign investors would be attracted by higher rates of return.

Basic economics tells us that inflation occurs when a few things happen, top of which is rising prices and too much money chasing too few goods. Others include, a rise in the cost of producing goods and services, demand exceeding supply, wages rising leading to increased purchasing power, natural disasters impacting farming or production, conflicts disrupting supply lines or when tax cuts lead to higher purchasing power.

Almost all of these have happened since 2023 and led to an increase in headline inflation something Cardoso also noted at that MPC briefing. In his words “members note the continued rise in headline inflation driven largely by food prices because of supply shortages and high cost of logistics and distribution.”

The last bit was, of course, a euphemism for high transport costs exacerbated by the increase in the fuel price.

So, curbing borrowing which leads to more money in circulation is clearly a step in the right direction.

While it is true that a high interest rate will discourage borrowing and potentially impact productive activities, the point should also be stressed that all over the world, the interest rate and inflation rate are connected because central bankers realize that the interest rate should usually be higher than the rate of inflation if prices are to stay stable which is what Yemi Cardoso is trying to do – keep prices stable and low and restore the purchasing power of ordinary Nigerians who are the most impacted.

A quick look at statistics from Statista will show us a trend for inflation vs interest rates for a few countries as at July 2024:

Australia, inflation rate of 3.5% and interest rate of 4.35%

Brazil: inflation rate of 4.5% and interest rate of 9.5%

Canada: inflation rate of 2.5% and interest rate of 4.5%

Russia: inflation rate of 9.1% and interest rate of 16%

UK: inflation rate of 2.2% and interest rate of 5.25%

US: inflation rate of 2.9% and interest rate of 5.38%

Now, if central banks the world over have realised that interest rates must be higher than the inflation rate why do we scream blue murder each time the MPC raises the MPR?

The answer I believe is because we are looking at high double digits. Back in the mid noughties when I worked at Zenith bank interest rates were around 12 and 13% and I remember that fixed deposits used to attract less than 10% returns. So, if the MPR had been moved by 200 basis points from 12.75 to 14.75% there would be not so much hoopla.

To underline this point, let us go back to 2006. Resolutions from the MPC Meeting of February 14, 2006 included: “Resolved to work towards maintaining single digit (core) inflation… MRR will be maintained at 13% in line with the anti-inflation stance of the MPC.” This shows that the resort to MRR or MPR as an inflation monitoring tool is historic and pre-dated Cardoso and his team who have set an inflation target of 21.4% in the short term.

Another point that needs to be made is that if interest rates remain lower than the rate of inflation in an inflationary environment such as we have presently, it could be an invitation to financial rascality where loans are obtained and used for what they were not intended for.

READ ALSO:

- Okey Bakassi Says Polygamy Best Form Of Marriage For Africa

- UNICEF donates 720,000-litre oxygen plant to Yobe

- G7 foreign ministers to address Netanyahu’s ICC warrant at meeting

- Ponzi schemes, SEC promises to take action

- Council to arrest parents children hawking during school hours

And that point leads me back to my days as a researcher at Zenith bank. Back then, in analyzing and providing opinions on feasibility studies, I was often mystified when I read the financials presented by start-ups seeking loans. A service oriented business would, for instance, apply for N60m take off loan and present line items for its sunk costs showing – business registration, legal, rent, office equipment, salaries and wages etc. But then you would often discover that N25m had been allotted to be used for “buying cars for marketing.”

My boss back then always told me that such depreciating assets must never be allotted more than 20%!

The issue was that in those days, with interest rate at about 10%, the temptation to be imprudent was high. This is what Yemi Cardoso is fighting to stop in an era of high inflation. Whatever is borrowed now must be applied judiciously to productive activity.

So, do we expect the MPR to go higher? My view is that it should. The MPR must correlate in some particular with the rate of inflation and as the CBN governor noted at that Harvard Club event “in the face of economic challenges, it is imperative to focus on core objectives—restoring the credibility of the institution, building trust in the financial system, and, most critically, containing inflation. These are not just strategic goals; they are foundational to any meaningful recovery.”

In concluding, I must return to a submission I made in a previous intervention; for the economy to grow and the gains become apparent in the medium to long term, there must be a convergence of both monetary and fiscal policies? Monetary policy is not a silver bullet even though it seems to be working with headline inflation dropping and the gap between the official and parallel markets contracting. Interesting days lie ahead.

**Toni Kan is a PR expert and financial analyst.