On September 22, 2024 Yemi Cardoso will mark one year in office as the governor of the Central Bank of Nigeria at a time of unprecedented economic headwinds. What will his scorecard look like?

A while back, I was discussing with a few friends and as is the case where one or two or more Nigerians are gathered, the discussion segued naturally to the economy. It was school fees season and three of us have children schooling abroad.

At some point, one of my friends blurted out. “Naira is now N1,580 to the dollar. What exactly is Cardoso doing at the CBN?”

This particular friend holds an MBA from a foreign university and runs two businesses in Nigeria so I was quite surprised when he reduced the functions of the CBN governor to just managing the value of the naira.

But it was not surprising. Speak to ten Nigerians and they will express almost the same sentiments. What is Cardoso doing if he can’t manage the foreign exchange rate?

The question is a valid one but also a bit reductionist because the job of a CBN governor extends beyond foreign exchange management, to include formulation and implementation of monetary policy, ensuring financial stability, reserve management, banking regulations, setting interest rates and more.

So, reducing the job description of the CBN governor to just one item in a long shopping list would be akin to a man who spends his time brushing one single tooth out of 32.

Why is foreign exchange management so important to Nigerians? Well, the short answer is that it makes news and impacts us in a lot of ways – school fees, medical care, travel, cost of goods, etc.

The naira has been making serious news since Cardoso assumed the mantle at CBN. According to the most recent World Bank’s biannual publication, Nigerian Development Update, of December 2023, the naira “depreciated against the US dollar by approximately 41% in the official market and by about 30% in the parallel market” between June and December 2023.

This was in the wake of the liberalization of the foreign exchange market or (managed) floating of the naira because the CBN is still intervening to reduce the pressure on the naira. Why was the naira floated? It was to ensure that the naira finds its true value, checkmate round tripping and remove speculative arbitrage. The ultimate aim is to achieve parity through a positive contraction in the gulf between the official and parallel market rates. But this cannot be achieved overnight.

Yemi Cardoso admitted as much when he appeared before the House of Reps in February 2024. Acknowledging that foreign exchange management is a key part of his remit, he also noted that ““the genuine issue impacting the exchange rate is the simultaneous decrease in the supply of, and increase in the demand for, dollars. It also seems that the task of stabilising the exchange rate, while an official mandate of the CBN, would necessitate efforts beyond the apex bank itself.”

This is because boosting the value of the naira against the dollar depends on more than just the CBN defending the naira. There are other factors; oil prices in the international commodity market, a productive economy, growth in exports both oil and non-oil products, increase in foreign reserves and dollar availability which often receives a boost from diaspora remittances, a reduction in the demand for dollars and containment of inflation.

The CBN is working to make these happen and Cardoso hit the ground running by taking quick key decisions; mandated banks to adhere to Net Open Position (NOP) limits to discourage hedging and prevent excessive holding of foreign currency assets. He also ensured that backlogs of unpaid forex obligations were cleared.

But the fact remains that for an economy to grow and the local currency gain strength there must be a convergence of both monetary and fiscal policies? Monetary policy is not a silver bullet.

We saw some movement recently on the fiscal front. The first domestic dollar denominated bond was oversubscribed by 180%. Planned to raise $500 million, the bond secured $900 million in commitments.

While the oversubscription surprised analysts and underlined investors’ confidence not just in the ongoing economic reforms but Nigeria’s economic stability and growth prospects there are concerns that the bond should have been targeted more at diaspora remittances instead of domestic dollar deposits as it put demand pressure on the dollar in local supply and the CBN may have to cough up about $200m in 5 years with interest rates of 9% per annum for bond holders.

While the jury is still out on the bond’s final impact on the economy, the fact remains that seamless fiscal and monetary synergy is required to get us out of the doldrums.

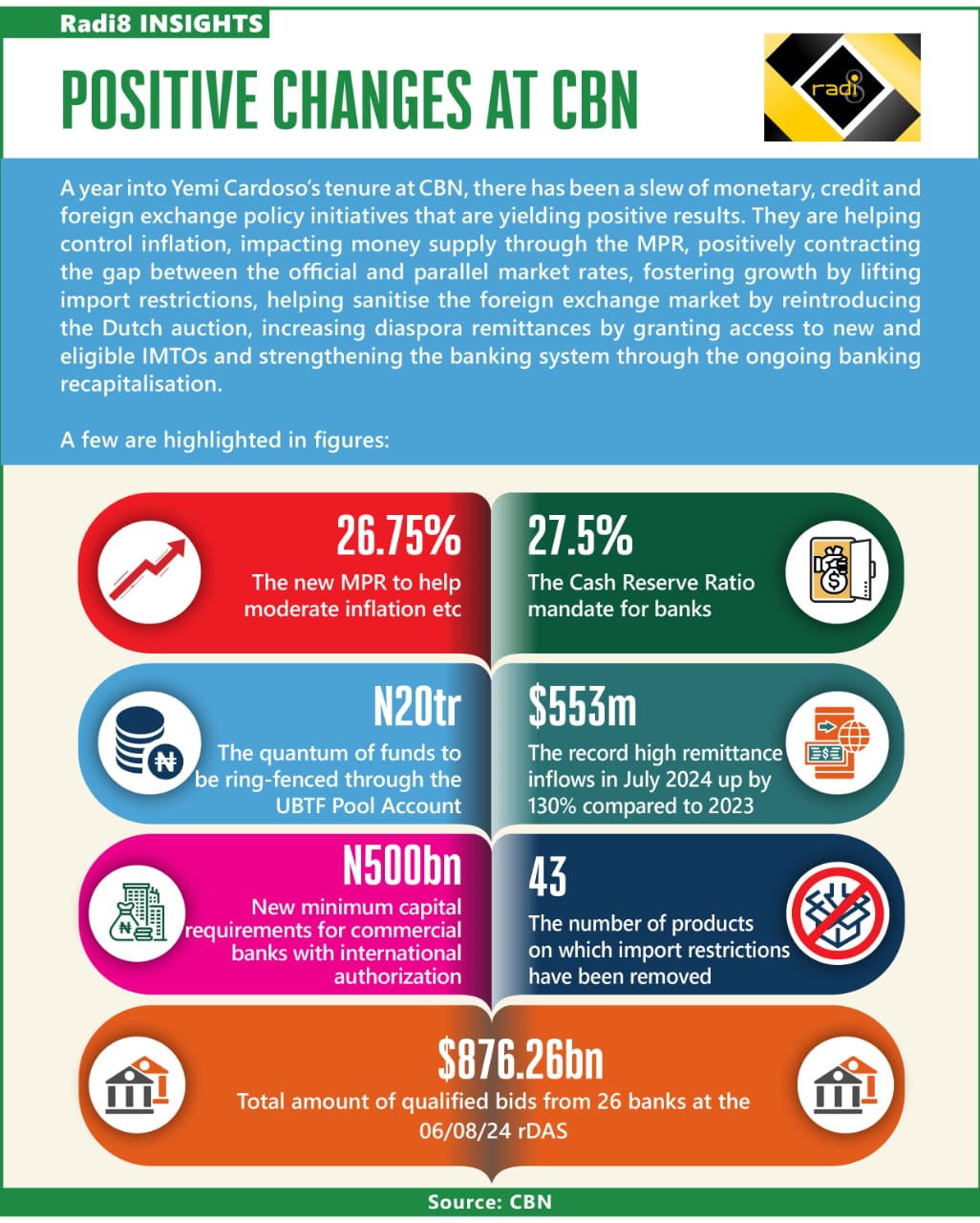

Prior to this, the CBN under Cardoso had recorded an all-time high $553m diaspora remittance inflow in July 2024 up by 130% compared to 2023. That significant uptick was thanks to the CBN’s decision to grant access to new and eligible international money transfer operators (IMTOs) to trade on the official foreign exchange (FX) window, implementing a willing buyer-willing seller model, and enabling timely access to naira liquidity for IMTOs thereby enhancing liquidity in Nigeria’s FX market.

There have been other monetary, credit and foreign exchange policy initiatives introduced by Cardoso which are yielding positive results.

The Monetary Policy Rate was raised to 26.75% in July 2024, the 4th time in seven months. The increase which impacts the cost of borrowing while encouraging savings is to moderate inflation while ensuring price stability. While analysts have argued that it could stifle productive activity, the increase in the MPR appears to be having a salutary effect on month on month inflation with inflation dropping by 1.25% compared to July according to the Nigerian Bureau of Statistics (NBS).

To address the expressed concerns the CBN has lifted import restrictions on 43 goods with the aim of achieving stability and fostering growth because cheaper imported inputs will lead to local production which will in turn boost employment as closed factories re-open and consumers will benefit from more affordable imported retail products.

The restrictions which had been in place for about eight years was ostensibly to conserve forex and encourage local production as importers were barred from using forex sourced from the official market to import the goods. But the reverse seemed to be the case as the imports continued with importers sourcing their forex from the parallel market thereby “exerting additional demand pressure on the parallel market, widening the gap with the official rate and permanently segmenting the market.”

To reduce demand pressure in the foreign exchange market and promote price discovery, the CBN re-introduced the retail Dutch Auction System (rDAS). The Dutch auction mechanism is not new having been applied previously in 1987, 1990 and from 2002 – 2006. The system is helping sanitise the foreign exchange market by allowing for an objective evaluation of forex demand and supply ensuring that demand is for end users. Predicated on the volume of forex available for sale, rDAS, by giving forward guidance, promotes forex stability.

On August 6, 2024 $1.18bn bids were received from 32 banks with total bids of $876.26bn from 26 banks qualifying while $313.69 from six banks were disqualified for various reasons ranging from late submission, wrong template to unverifiable forms. In the pursuit of transparency, all the bids have been published on the CBN website. The effect of the return of rDAS was felt immediately with an appreciation in value.

Aside sale to banks through rDAS, the CBN is also ensuring forex availability to registered and qualified Bureaux de Change operators.

Another key initiative was the announcement that the CBN would no longer indulge the FG’s Ways and Means appetite until the previous loans, put at N18.16 trillion which is 40% higher than total money in circulation as at 2023 are repaid. Cardoso said the bank will insist on following the rules which states that the CBN cannot advance the federal government more than 5% of revenue earned in the previous year. Bold and fraught with political implications, it is meant to reduce currency in circulation and so moderate inflationary pressure.

Cardoso’s attempt to moderate government spending and fiscal dominance has already received political push back with the National Assembly approving an increase of that threshold from 5 to 10% of annual revenue.

In terms of its regulatory functions as banker to the banks, the CBN is focused on ensuring the financial stability of Nigerian banks. It is strengthening the banking system through the upward review of the minimum capital requirements, increase in the Cash Reserve Ratio (CRR) and ring fencing of the banking system through the Unclaimed Balances Trust Fund (UBTF) Pool Account.

According to the recapitalisation guideline issued on March 28, 2024, commercial banks with international authorization are now required to have a new minimum capital of N500bn which the CBN says will “enhance their resilience, solvency and capacity to continue to support the growth of the Nigerian economy.” While the targets differ based on the bank’s licence, the recapitalisation exercise is supposed to take place over 24 months and conclude on March 31, 2026. At the time of writing, share raise offers by Fidelity, Access and Guaranty Trust have been oversubscribed.

The increase of the CRR to 27.5% will help ensure that Nigerian banks are cash positive while reducing the amount of cash in circulation thereby helping achieve the CBN’s inflation moderation agenda.

The Unclaimed Balances Trust Fund (UBTF) Pool Account will warehouse “unclaimed balances in eligible accounts” helping to protect the banking system by limiting incidents of fraud to which dormant accounts are susceptible.

READ ALSO:

- Ex-BBN Star Phyna Kicked Out Of Restaurant Over Indecent Dressing In Lagos (Video)

- Court dissolve 45-year-old marriage over alleged infidelity

- Peace cornerstone for national development – Badaru

- Leaders of Faith and Culture Unite to Mark 16 Days of Activism Against Gender-Based Violence

- Daniel Regha Urges Dangote To Sell Fuel For N300

Finally to ensure that the policy initiatives are communicated and understood, the CBN is encouraging transparency with a return to full disclosure in the form of regular publications of reports and data. According to the CBN this is to reaffirm its “commitment to fostering transparency and accountability in the Nigerian economy.” It will also complement the data available from other sources like the NBS thus providing Nigerians a better view of the economy.

But is it working and is any one taking notice? To return again to the question we posed at the beginning; what will Cardoso’s scorecard look like?

While the naira’s battle against the dollar will dominate discourse, his adoption of proactive forex policies, regulatory initiatives and a robust inflation-targeting framework indicate that Cardoso has shown himself as a CBN governor capable of coming up with and translating strategic initiatives into actionable outcomes.

One year into his tenure, the CBN’s target inflation rate of 21.4% has not been achieved and the naira is still on the back foot relative to the dollar, but time may well be on his side but not so for impatient Nigerians eager to see quick wins.

Toni Kan, is a PR expert and financial analyst.